Why the Fed's Delay in Cutting Rates Is a Mistake VIEW IN BROWSER Every Fed Chair gets remembered for something. Paul Volcker tamed inflation in the 1980s. Alan Greenspan presided over the dot-com boom and bust in the 1990s through the early 2000s. Ben Bernanke battled the financial crisis. Janet Yellen’s time was short-lived, but she was the first female chief of the Federal Reserve. As for Jerome Powell? If President Trump has anything to say about, his entire legacy will boil down to two words: too late. And you know what? He has a point. Powell was too late to hike key interest rates when inflation was building during the pandemic in 2021. Too late to admit that “transitory” wasn’t the right call when describing inflation and the Fed’s lack of action. Mind you, this was after the federal government unleashed a historic wave of stimulus. Not to mention the fact that containerships dotted the horizon in most ports across the country in late 2021 when supply chains were messed up around the world. And now? Powell is too late again – this time to cut rates. We saw more of that story unfold this week. On Wednesday, the Fed held rates steady for the eighth straight meeting, despite persistent signs that inflation is easing and growth is starting to slow. In today’s Market 360, I’ll recap this week’s Fed meeting and explain my frustration with the Fed. I’ll also detail why the warning signs are flashing in the data. Then, we’ll go over the latest inflation numbers, which were released today. And finally, I’ll offer my take on what comes next – and how you can best position yourself to profit. | Recommended Link | | | | If you missed Bitcoin in 2011, Tesla in 2012, or NVIDIA in 2016, you know the sting of regret…Now the master trader Jeff Clark has uncovered a new opportunity. He calls it “Crossfire” — and it could hand you gains of as much as 1,285% in as little as two days. Don’t let this become another “what-if” moment. Watch his free briefing now. |  | | Powell & Co. Keep Rates Steady Let’s start with the Federal Open Market Committee (FOMC) meeting that wrapped up this Wednesday. The Fed held interest rates steady – again. That makes the fifth meeting in a row with no change, leaving the fed funds rate stuck in a range of 4.25% - 4.50% since December 2024. Now, on paper, Powell and the rest of the FOMC are saying the right things: they’re “data dependent,” they’ll “remain vigilant,” and so on. So, the good news is the Fed acknowledged the economy is softer, but it’s not enough to cut rates yet. I should add that some members of the FOMC see the light. Fed governors Christopher Waller and Michelle Bowman dissented in the vote. That’s a big deal, because it’s the first time two voting members have split with Fed leadership in three decades. Now, before I go any further, I want to be blunt about something. Most of the Fed is living in a delusional world. They’re looking for an inflation bogeyman that doesn’t exist – and in the process, they’re ignoring the signals right in front of them. But before I go any further, let’s dive into this week’s inflation numbers. Then, hopefully, you’ll see what I mean. What the PCE Report Really Tells Us The Personal Consumption Expenditures (PCE) index report was released this morning. Now, this is the Fed’s favorite inflation gauge. Our central bank has expressed in the past that it would like to see it clock in at 2%, especially with regard to “core” inflation. Core PCE, which strips out food and energy, rose 0.3% in June. Economists were looking for 0.2%, and it’s also the biggest monthly jump since January. On a year-over-year basis, core PCE is now running at 2.8% – exactly where it was the month before, when accounting for the upward revision in this report. So, while it’s not ideal, it’s not accelerating, either. Now, let’s dig into the underlying economic data from the same report: - Real personal spending – which adjusts for inflation – rose 0.3%, a modest bounce after May’s drop of 0.3%. But it still came in below economists’ forecasts.

- Personal income also rose 0.3%, recovering from a 0.4% decline the month before. Again, nothing to celebrate. Just a mild rebound.

- Savings rates dipped slightly, suggesting consumers are leaning on credit or drawing down savings to keep up with expenses.

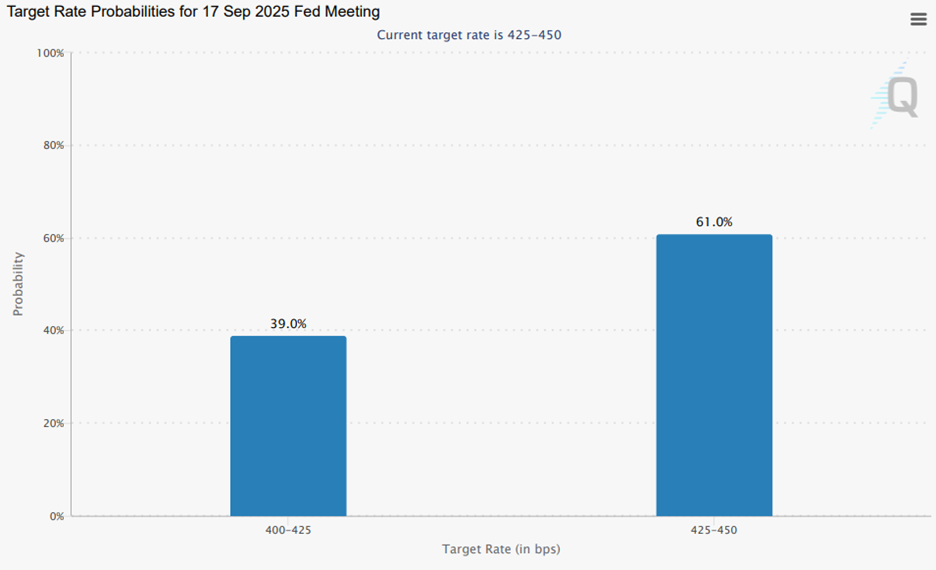

So, yes, we did have a slight surprise in the numbers with this report. But the reality is that inflation is not running wild. Meanwhile, growth is starting to sputter. What's Really Going on Behind the Data Aside from this week’s report, inflation has been consistently coming in below expectations. For example, the Consumer Price Index (CPI) has come in below what economists expected for five straight months. I’ve been pointing this out again and again – and yet the Fed keeps ignoring it. Why is that happening? One is that there’s deflation in China. Two, there was a buildup of inventories trying to beat the tariffs. Three, economies around the world are weak, and it is very hard to increase prices. Four, the dollar is getting its mojo back – and its appreciation in the next year or so is going to more than offset the tariffs. Period. Still, Jerome Powell insists there’s “a long way to go.” He even said during his press conference that it’s “too early” to understand the impact of tariffs, as if he’s waiting for some phantom inflation spike to justify keeping rates high. But the reality is that nearly all of our inflation in America is related to real estate. And real estate prices are getting slashed across most of the country as we speak. There’s a glut of rental properties now, too. So, hopefully, the owner’s equivalent rent component in the CPI report will crack soon. And when it does, inflation could fall well below the Fed’s 2% target rate. Another reason we need to be cutting rates is the fact that global interest rates are falling. The European Central Bank is cutting rates. The Bank of England is expected to follow. Even China, which has its own mess to deal with, is slashing rates. That leaves us with some of the highest real rates in the developed world. And that has consequences. It strengthens the dollar (which isn’t all bad), but it also creates distortions. Growth starts to slow. Earnings start to wobble. And capital starts looking for safer, more productive ground. Looking Ahead In the wake of the Fed meeting and the PCE data, the market got the message. According to the CME FedWatch Tool, there’s now a 61% chance the Fed holds rates steady – up from just 40% a week ago, and 5% a month ago.  But here’s the bottom line... The Fed is squinting at the data through the wrong lens. They need to cut in September, again in December, and four more times next year. They need to get the federal funds rate down to about 3%. And if they keep waiting, they risk breaking something. The Bigger Picture for Investors So, what does all this mean? It means the Fed is behind the curve – again. But this time, markets aren’t going to wait around. Smart money is already repositioning. And a quiet policy shift from Washington is about to accelerate that trend even more. Earlier this year, President Trump signed a directive that laid the groundwork for a new kind of national investment strategy. Even though it hasn’t made headlines yet, I believe it’s one of the most important federal initiatives of the past decade. That’s because, in short, I believe it’s going to lead to the creation of the first-ever sovereign wealth fund in the U.S. So, instead of taxing or borrowing more, the MAGA Fund taps into assets the government already owns – land, resources, infrastructure – and begins deploying capital into companies strategically aligned with national priorities. And right now, a select group of public companies is already benefiting from this shift. I just released a new report with all the details – and I want you to see it for yourself. Click here now to watch my full briefing and learn how you can position your portfolio now. Sincerely, | .png)

.png)

No comments:

Post a Comment